This month in Digital Assets

May 2022

Once a month our team summarizes here the market movements and what we have been following for our client and ourselves. We have hand-selected what we believe to be must-reads of this month to ensure you are all caught up on the most recent developments. Articles are grouped per region to facilitate your pick based on interest.

The Crash of UST, The Fall of Terra and Flight from Other Stablecoins

One of the biggest stablecoin by market cap crashed at the beginning of the month - Terra’s UST stablecoin. This event confirmed concerns already raised by numerous governments and central banks regarding the risks of stablecoins on financial stability, such as the U.S. FED, the Bank of England, the European Central Bank and the South Korean government, to name only a few. UST’s crash had and still has significant repercussions over the stablecoins and broader crypto-currency market, reinforcing the relevance of a regulatory framework, as already proposed by various jurisdictions, to extend explicitly some existing regulations to crypto-assets and propose new ones to fill-in the existing gaps - particularly as the existing financial system becomes increasingly interconnected and integrated with digital assets.

Stablecoins are not without risks, nor stable, as the name would imply; A growing body of knowledge has documented the volatility of stablecoins (see Region North America: “The Fed cites its concern about stablecoins in its latest Financial Stability Report” for more details), but more research is needed to understand factors impacting this class of digital assets. Yet, it’s important to remember that stablecoins only entered the scene in 2014 with the BitUSD. The process of innovation being iterative, stablecoins, and their various mechanisms, are no exception. Only through a thorough understanding of the risk exposure of crypto assets, and what systemic and idiosyncratic factors could trigger and reinforce the spread out of the negative impact to multiple crypto ecosystems can adequate regulatory frameworks be put in place without hindering the innovation.

The fact that the crash did not stop the United Kingdom from moving forward with the legalization of stablecoins as a form of payment suggests that, at least some governments, understand the importance of striking a balance (see below “UK Treasury en route to legalizing stablecoins amid Terra’s UST crash” for more details).

The Fall of Terra: A Timeline of the Meteoric Rise and Crash of UST and LUNA

[Coindesk]

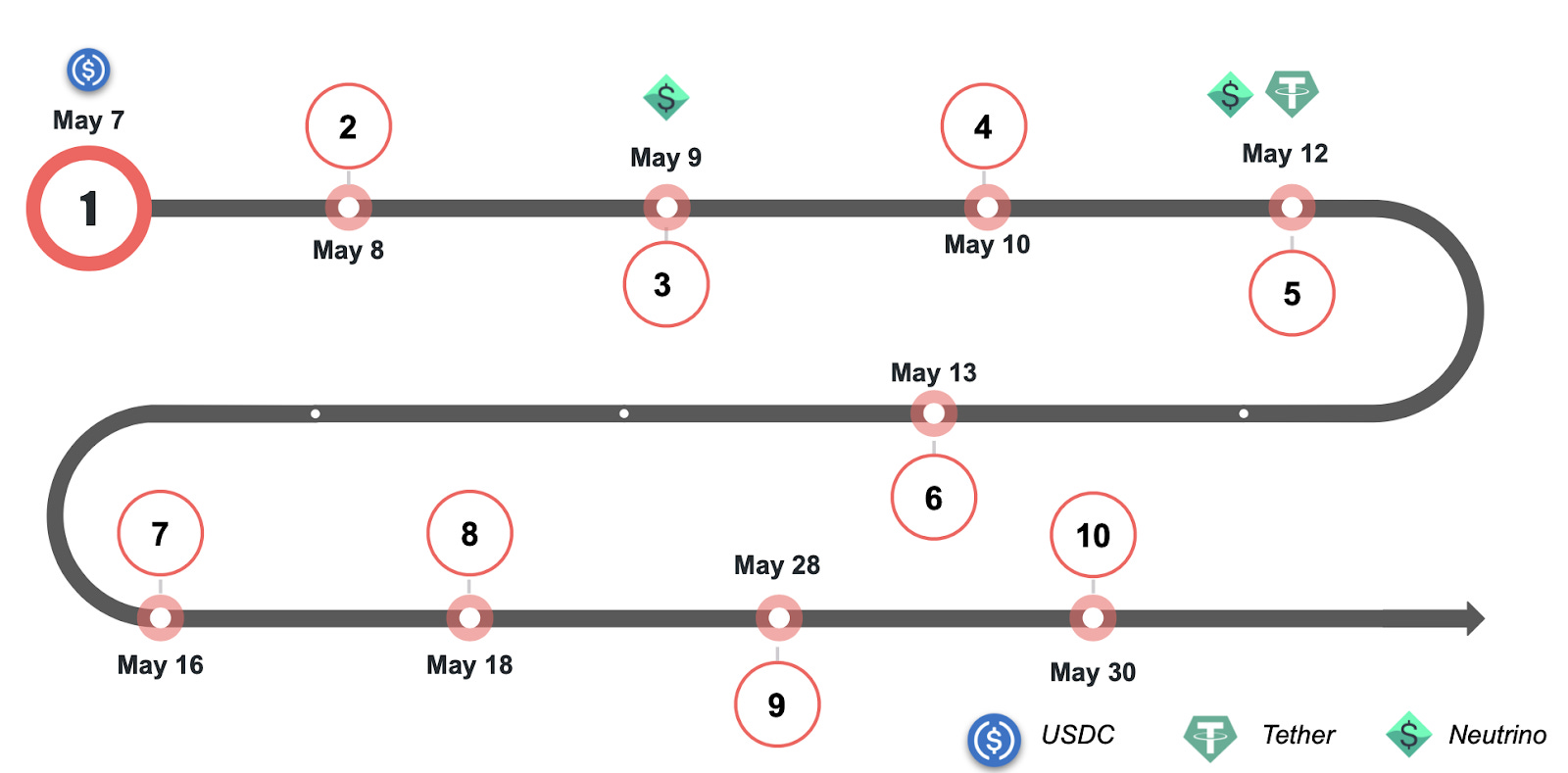

In early May, the third largest stablecoin in terms of market capitalization, UST, lost its peg, resulting in numerous impacts on the entire crypto market. UST is Terra's algorithmic stablecoin which is backed by Terra's native coin, Luna (Refer to the attached BlockZero document for an overview of the different types of stablecoins). Indeed, on May 8, Terra's stablecoin lost its peg to the U.S. dollar as its value dropped, a decline that kept on the next day, where the UST dropped to 35 cents. Recall that a stablecoin is supposed to be stable, by maintaining its value at $1 since it is tied to the price of a fiat currency, such as the U.S. dollar. The algorithm of UST that ensured its peg worked fine for as long as Terra had value on the market. However, as the price of luna continued to fall, so did Terra.

Below, we provide an overview of the key events of the UST descent, resembling the confidence crisis that typically precedes bank runs.

For more details on Terra and stablecoin, we invite you to access this short document by Blockzero

See this link for event details:

https://www.coindesk.com/learn/the-fall-of-terra-a-timeline-of-the-meteoric-rise-and-crash-of-ust-and-luna/

https://www.necn.com/news/business/money-report/worlds-biggest-stablecoin-regains-dollar-peg-after-3-billion-in-withdrawals/2738134/

Why Crypto’s bruising comedown matters - it has prompted flight from some stablecoins into others

[The Economist]

One of the key characteristics of a run (be it a bank or investment type) is the sudden and massive contagious effect it has on other investors and on assets (or companies, countries, etc.) perceived as similar in terms of risk. This is especially true if those similar risks are not covered or not as well as necessary. This is a main issue with crypto and stablecoins due to the lack of regulation in the sector.

The repercussions of UST’s crash were beyond just Terra, and caused other stablecoins perceived as similar in terms of risks to lose their peg as investors fled to “safer” alternatives. Of importance, Tether, the oldest and largest stablecoin in terms of market cap also lost its peg. The likely cause: the lack of transparency regarding how exactly Tether is backed 100% by cash, Treasuries and corporate debt, contrarily to USD Coin which is backed by cash and Treasuries, AND regularly publishes its audits.

Tether is more than a financial bridge between conventional money and crypto, but also between crypto (crypto pairs) traded on some of the largest exchanges. As such, should it crash, the impact would be “much more catastrophic” than for Terra’s.

https://www.economist.com/finance-and-economics/2022/05/19/why-cryptos-bruising-comedown-matters

UK Treasury en route to legalizing stablecoins amid Terra’s UST crash

[CoinTelegraph]

Meanwhile, the United Kingdom’s Department of Treasury has decided to go ahead with the recently announced legalization of stablecoin as a means of payment within the UK. This decision comes with the UK treasury's desire to continue to develop and promote cutting edge technology and innovation in the financial services industry.

The Treasury's plan does not include the legalization of algorithmic stablecoins (i.e UST), but rather intends to favor stablecoins that are peg 1:1 to fiat currency. Nonetheless, the legalization of this type of stablecoins will allow the government to strike a balance while it continues to learn about stablecoins and while the crypto industry continues to innovate, learning from the May 2022 crash.

https://cointelegraph.com/news/uk-treasury-en-route-to-legalizing-stablecoins-amid-terra-s-ust-crash

REGION: NORTH AMERICA

The Fed cites its concern about stablecoins in its latest Financial Stability Report

[Cointelegraph, U.S. Federal Reserve Report]

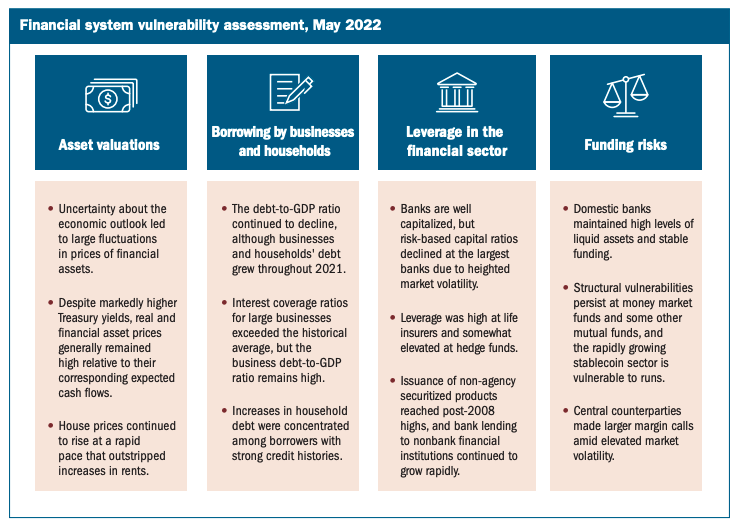

At the very same time the UST stablecoin began to lose its peg, on May 9th specifically, the U.S. Federal Reserve Board issued its semi-annual Financial Stability report, which presents its current assessment of the resilience of the U.S. financial system through an assessment of vulnerabilities related to asset valuations, borrowing, financial sector leverage and funding risks, along with near-time risks that could interact with these.

Of interest, the rapidly growing stablecoins market, which reached a value of USD 180 billion as of March 2022 was singled out, along some money market funds, as particularly vulnerable to runs. The report pointed out that stablecoins, which were designed to reduce price volatility through the various mechanisms described earlier, face redemption risks that are “similar to those of prime and tax-exempt MMFs.” (FRB, 2022, p.42) This is due to the fact that, for the most part, stablecoins are backed by assets that may lose value or become illiquid during times of stress. This risk can be exacerbated by 1) a lack of transparency with regards to the riskiness and liquidity of the assets used to back the stablecoins; and 2) increased volatility in demand for stablecoins due to the growing use of stablecoins to meet margin requirements for levered trading in other cryptocurrencies.

While much remains unknown, there is a growing number of academic research that aims to better understand the stability of stablecoins (or lack thereof) and the measures that must be taken to minimize its vulnerabilities are being researched. For instance, Baur and Hoang (2021) and Grobys & al. (2021) showed that contrary to popular beliefs, stablecoins are not stable, and that their volatilities are erratic (vs that of Bitcoin being well-behaved, statistically). Moreover, by being pegged to the U.S. dollar, stablecoins’ volatility is constrained. However, the authors point out the work of Taleb (2012, p. 106) that indicated that artificially suppressing a system, the latter can become “not only fragile but visibly reveal little or no risks even though such risks are latently growing.” Moreover, Grobys & al. (2021) further demonstrated that Bitcoin volatility is a fundamental factor that drives the volatilities of stablecoins.

As people await the results of President Bidden’s Executive Order, notably on the impact to the financial stability of stablecoins and how to best regulate these assets, we look forward to observing whether nations will simply act by banning stablecoins or rather looking at mechanisms to ensure the financial stability of the financial markets while allowing for innovation.

https://cointelegraph.com/news/the-fed-cites-worries-about-stablecoin-in-its-latest-financial-stability-report

https://www.federalreserve.gov/publications/files/financial-stability-report-20220509.pdf

Grobys, K., Junttila, J., Kolari, J.W., and Sapkota, N. (2021). On the stability of stablecoins. The Journal of Empirical Finance, 64, p. 207-223.

Baur, D.G., Hoang, L.T. (2021b). A crypto safe haven against Bitcoin. Finance Res. Lett. 38, 101431.

Taleb, N.N., 2012. Antifragile. Penguin Books, London.

Coinbase Enters Fortune 500 List of Biggest U.S. Companies

[Coindesk, Fortune Rankings]

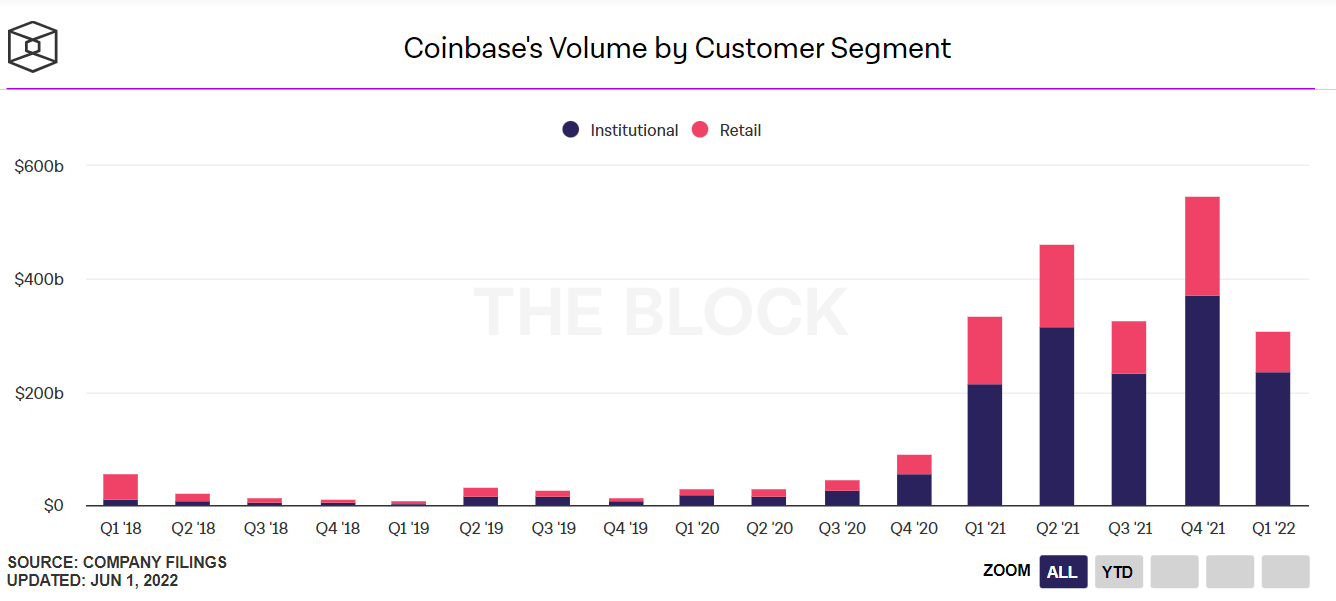

On May 24th, Coinbase, the largest crypto exchange globally, became the first crypto company to join the Fortune 500 List, ranking 437th.

The list accounts for two-thirds of U.S. gross domestic product, with revenue totaling $16.1 trillion. Coinbase recorded revenues of $7.8 billion in fiscal year 2021, representing an impressive 513.7% growth year over year; a growth which attests to the growing market of digital assets.

However, earlier in May 2022, Coinbase shares fell by nearly 16% as the company announced Q1 2022 earnings of $1.17 million, falling short of the average analysts’ estimates of $1.5 billion. Trading volumes for Q1 were 44% lower compared to the previous quarter. Whether or not Coinbase will remain part of the Fortune 500 listing for 2022 is the question - particularly as the U.S. government and other jurisdictions are looking to increase crypto regulation. The firm’s commitment to innovate and remain a leader in that space, however, makes it unlikely it would lose this position - at least in the near future.

Recall that as of last October, Coinbase had over 2 million people on its white list for its upcoming NFT marketplace, whereas the largest NFT marketplace, OpenSea, had only 300 000 users at the time. Moreover, we have documented several times the general trend we have observed, whereby the traditional financial sector is merging with that of digital assets. Coinbase is no exception. Although the company doesn’t have a plan yet to offer securities, it filed a shelf registration statement with the Securities and exchange commission (SEC) last year as to broaden its possibilities in the future. Lastly, Coinbase’s shift of getting more institutional clients might have helped it to increase trading volume and drive up revenue and enable its move to a Fortune 500 company.

Source graphic: https://www.theblockresearch.com/data/crypto-markets/public-companies

https://www.coindesk.com/business/2022/05/24/coinbase-enters-fortune-500-list-of-biggest-us-companies/

https://www.coindesk.com/business/2022/05/10/coinbase-q1-revenue-misses-estimate-trading-volumes-fall-from-previous-quarter/

https://www.benzinga.com/markets/cryptocurrency/21/10/23471861/coinbase-passes-2-million-registrations-for-nft-platform-company-shares-plans-for-launch

Economic well-being of U.S. households in 2021 - May 2022

[U.S. Federal Reserve Report]

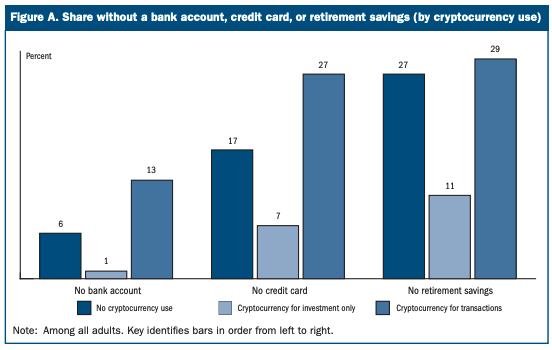

The Federal Reserve Board issued another important report this month - the Economic Well-Being of U.S. Households in 2021 - that shed some light on cryptocurrency adoption in the United States. The survey, which interviewed over 11,000 individuals in October and November 2021 revealed that 12% of respondents held or used cryptocurrency, with the majority holding it as an investment (11%) vs a minority using it for payment / purchase (2%) or to send money to friend/family (1%).

Interestingly, the survey revealed different demographic characteristics regarding the use/hold of cryptocurrency. 46% of respondents holding cryptocurrency for investment purposes only had income of 100,000 USD or more vs 29% having income lower than 50,000. These individuals almost always had traditional banking accounts and typically had other retirement savings (see figure below). In contrast, nearly 60% of adults who used cryptocurrencies for transaction purposes had income of less than 50,000 USD. They were also more likely to lack a bank account (13% vs 6% of adults who did not use cryptocurrency) and not have a credit card (27% vs 17% of non-users).

Lastly, the report provides recent statistics of the share of unbanked, underbanked and fully banked adults. While these statistics remained essentially the same between 2020 and 2021, the longer-term trend shows a 7 percentage point decrease in the underbanked rate over the past 6 years. The report outlines that although most of that decline might be attributed to a decrease in the use of alternative financial services, these statistics do not necessarily indicate an improvement in financial inclusion, particularly as the market for financial products and services, notably in the digital space, has evolved over the recent years. These statistics are necessarily of interest as the U.S. proceeds with its assessment of the benefits (and risks) associated with digital assets, particularly the relevance of a U.S. Central Bank Digital Currency (CBDC) or digital U.S. dollar, but also how to best regulate this market without hindering financial inclusion and innovation.

https://www.federalreserve.gov/publications/files/2021-report-economic-well-being-us-households-202205.pdf (p. 43-46)

REGION: EUROPE

Decrypting financial stability risks in crypto-asset markets

[European Central Bank Report]

The European Central Bank released as part of its Financial Stability Review and analysis that outlines the financial stability risks in crypto-asset markets, with a focus on unbacked crypto-assets and DeFi (and therefore abstracts from stablecoins). The article provides recent statistics on the growing demand from institutional and retail investors in the Eurozone. Notably, a survey conducted by Fidelity Digital Asset indicated that 56% of European institutional investors surveyed have some level of exposure to digital assets, a 11 percentage point increase from 2020. Moreover, a recent survey conducted by the ECB (for 6 large euro area countries) revealed that as many as 10% of households may own crypto assets.

However, what is most interesting is that it confirms what, intuitively, is already known from regulators: according to this survey, “higher income households are more likely to hold crypto-assets, with lower-income households more likely to hold crypto than middle-income households.” And, “respondents who scored either at the top level or bottom level in terms of financial literacy were highly likely to hold crypto-assets.” Hence, the importance for greater investor protection - at least, similarly to what would be expected in the traditional financial services sector. To that effect, the report outlines key consumer protection risks.

Lastly, the article’s narrative revolves principally around one theme, effectively arguing that while the risk to financial stability might not be significant at this point in time, as the market continues to grow and, importantly, as the convergence between the traditional financial sector and crypto assets continues, the interconnectedness will lead to greater systemic and financial stability risk. Financial stability implications would stem from the four transmission channels: wealth effects, confidence effects, financial sector exposures and the use of crypto assets as a form of payment. Lack of internal shock absorbers to provide liquidity at times of stress, the use of significant leverage (sometimes as much as 125 times the initial investment), margin trading, and relatively low Loan-to-Value ratios that do not consider the high volatility of crypto are all elements that contribute to this risk to financial stability.

Should the crypto industry prepare for increased regulatory oversight and requirements for sharing data (audited) with regulators? This article suggests so. While outlining the importance of a globally coordinated approach - similar to what President Bidden’s Executive Order indicated.

https://www.ecb.europa.eu/pub/financial-stability/fsr/special/html/ecb.fsrart202205_02~1cc6b111b4.en.html

Bitcoin mining in Norway gets the green light as the proposed ban rejected

[Cointelegraph, Canadian Blockchain Consortium]

In March 2022, a proposal to ban Bitcoin mining in Norway was suggested by the Norwegian Communist Party. The final decision was made in early May in the Norwegian Parliament, with a majority of votes against banning Bitcoin mining, which blocked the bill and gave the green light to Bitcoin mining. Norway's decision to give the green light to Bitcoin mining brings several economic benefits to the country, such as job creation, tax payments, etc.

Norway is not the only country where Bitcoin mining has had a lot of pressure from different political parties or governments in the last month. Indeed, New York State and Russia have also had their pitfalls due to regulation constraints. For instance, New York State regulators are currently looking at how to limit emissions-creating mining projects. While in Russia, sanctions have been issued by the U.S. Treasury Department for certain Western companies operating in Russia (i.e. BitRiver).

These various regulatory pitfalls demonstrate the importance of having greater regulatory clarity for mining operations. Moreover, although mining is energy intensive, not all energy is equal. Indeed, Norway uses 100% renewable energy for its mining operations, and the benefits of these are probably greater than the risks. For ways in which the digital asset mining industry is innovating to reduce their carbon footprint, and that of other industries, refer to our April newsletter.

https://cointelegraph.com/news/bitcoin-mining-in-norway-gets-the-green-light-as-the-proposed-ban-rejected

https://canadablockchain.readz.com/june-2022.pdf#10

REGION: MEA

Emirates Airline Plans To Add Bitcoin As A Payment Service

[Bitcoinist]

Emirates Airlines, one of the world’s largest airlines has shown intent to add crypto payments, offer NFTs for trading on the company’s website, and enable a metaverse platform. Emirates’ Chief Operating Officer (COO), Adel Ahmed Al-Redha, revealed that the firm will hire new staff for their metaverse and NFT ambitions. They expect to transform in their operations, training, and sales experience by making it interactive with a metaverse application. They are also looking to explore the application of blockchain technology in tracing airplane records. Additionally, the COO spoke about plans to add Bitcoin as a payment option as well.

Should Emirates Airlines succeed in deriving value, for the company and its clients, it may drive more such players in the airline industry and beyond to leverage the digital asset infrastructure to their advantage.

https://bitcoinist.com/emirates-airline-plans-to-accept-bitcoin-payments/

REGION: APAC

China: E-currency blossoming nationwide

[China Daily]

China’s central bank digital currency, known as the digital yuan or e-CNY, started trials in Shenzhen in October 2020 and recorded the equivalent of US$11.24 billion worth of transactions by the end of 2021. In April 2022, China broadened the range of public services and the number of cities included in its digital yuan pilot projects. Now the month of May was eventful, showing a trend toward greater social adoption.

Notably, the E-CNY subsidy programs are starting to pilot. On May 10th, 2022, one million yuan were granted for new electric vehicle buyers and another four million yuan of subsidy in form of e-CNY will be provided in the following months. Further societal acceptance can be shown through technology companies’ application and transaction numbers.

Alipay, one of the most popular mobile payment systems in China owned by Alibaba Group, launched a search function for e-CNY on May 5th, with which users can open CBDC yuan wallets and use CBDC for their online shopping. China’s leading online food delivery services provider Meituan indicated on May 7th that more than 4.4 million users have experimented with the e-CNY payments. E-retailer JD said transaction values of over 250 million e-CNY were completed on its platform from December 2020 to May 2022.

These several “first-time” attempts that occurred throughout the month of May along with the other new applications in the making point towards social adoption. It is interesting to see how versatile e-CNY can be for the Chinese government and the regulatory challenges officials will face during the pilot and implementation stages for the digital currency.

https://global.chinadaily.com.cn/a/202205/18/WS6284437fa310fd2b29e5d55a.html

https://forkast.news/headlines/china-expands-digital-yuan-public-service

https://www.reuters.com/markets/currencies/china-uses-digital-yuan-stimulate-virus-hit-consumption-2022-05-30/

RBI to take graded approach on CBDC, in line with monetary policy (and) financial stability

[Business Today]

The Reserve Bank of India (India’s Central Bank) announced that they would take a graded approach (Proof of Concept, pilots and the launch) towards the Digital Rupee (Central Bank Digital Currency (CBDC)). The CBDC will be in line with the monetary policy, financial stability and efficient operations of currency and payment systems. Even though the launch of the CBDC may happen in 2023, it may not be a full fledged launch and could be a Proof of Concept (PoC) or a closed pilot with a few financial institutions. It is also not known who the participants of this PoC or Pilot are going to be.

Since the deployment of a CBDC is specific to each country, such a graded approach is beneficial to allow the nation to test various scenarios and learn about any issues in advance before a full fledged launch.

https://www.businesstoday.in/crypto/story/rbi-to-take-graded-approach-on-cbdc-in-line-with-monetary-policy-financial-stability-335674-2022-05-30

REGION: SOUTH AMERICA

Central bankers (from 44 nations) bellow Bitcoin on El Salvador's Bitcoin Beach

[Cointelegraph]

32 central banks and 12 financial authorities (totaling 44 nations) met in El Salvador on May 16th, 2022 to discuss Bitcoin, financial inclusion, digital economy, banking the unbanked, and El Salvador’s Bitcoin rollout and its benefits in the country. Most of these 44 nations are from developing nations, including a few countries that are advancing on the CBDC front. It took 12 years for the first country (El Salvador) to adopt Bitcoin as legal tender, around 8 months for the second (Central African Republic), until April 2022 for the a Special Economic Zone in Honduras (Próspera ZEDE), and if Panama’s president signs their recent Bitcoin bill into law, then they will be the fourth.

Bitcoin as a form of monetary instrument is nascent and it being adopted as a legal tender may be risky due to its volatile nature. The countries that are considering Bitcoin as legal tender seem to have a low banked population and a poor payments infrastructure. Most importantly, the governments of such countries seem to be using the Bitcoin legal tender opportunity as a populist measure to gain popularity. This Bitcoin conference might motivate some of these countries to consider Bitcoin as legal tender. Whether this motivation is a move in the right direction seems to be questionable as the asset is yet to maintain its stability in value and prove its value to operate as a legal tender currency.

Bitcoin Lightning Network inaction. Source: Twitter

https://www.ft.com/content/8b68b0cd-230c-4e9b-aa66-84bdbe98c9e0

https://cointelegraph.com/news/central-bankers-bellow-bitcoin-on-el-salvador-s-bitcoin-beach

https://www.nasdaq.com/articles/president-nayib-bukele-announces-44-countries-to-meet-in-el-salvador-to-discuss-bitcoin

https://www.cnbc.com/2022/04/28/central-african-republic-adopts-bitcoin-as-legal-tender.html#:~:text=The%20Central%20African%20Republic%20has,the%20same%20step%20last%20year.

El Salvador Buys the Dip Again and Purchases 500 Bitcoin (BTC) Amid Crypto Crash

[Dailyhodl]

While the crypto market crashed in May, El Salvador continued to buy the dip on Bitcoin. The country bought 500 BTC at an average price of $30,744. As a result of this purchase, the country now has a total of 2,301 Bitcoin for $103 million as of May 2022.

Yet, many people in El Salvador are currently protesting against the BTC policy that was adopted by Bukele, the President of the country. In addition, the International Monetary Fund (IMF) has also criticized the policy because of the high risks of using Bitcoin on financial stability, financial integrity, as well as consumer protection.

Source: ARK Investment Management LLC, 2021

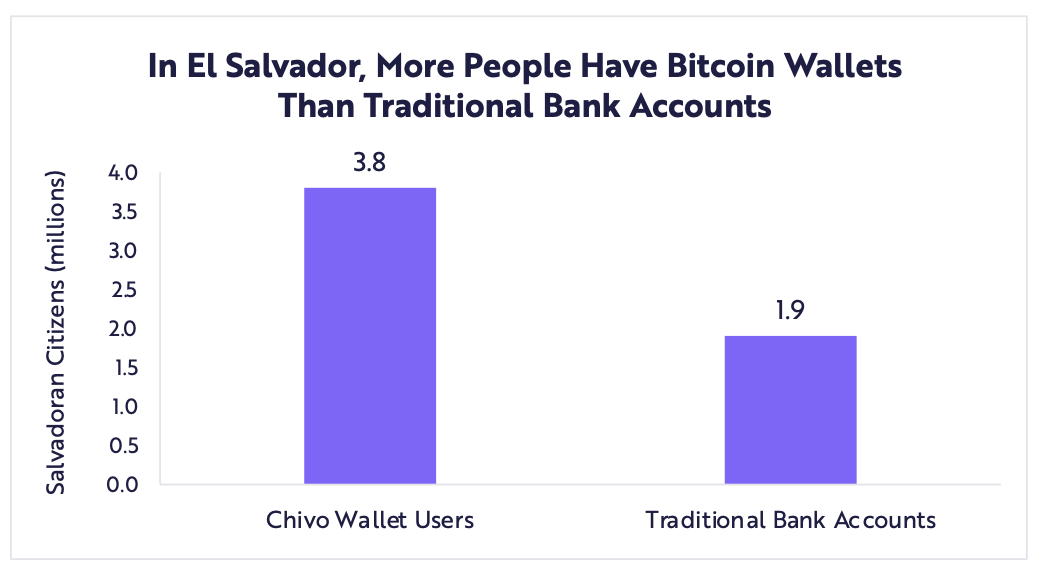

Recall that according to a study published by the National Bureau Of Economic Research last month, only 20% of El Salvadorians still use the Chivo Wallet, while about 3.8 million citizens have a Chivo account, which represents almost 84% of the citizens. Due to the low percentage of use, one might think that this represents a low adoption score. However, this does present a significant adoption in El Salvador especially when compared to the adoption of traditional financial services. In fact, according to Statista, only 29% of adults had a bank account in El Salvador in 2017.

https://dailyhodl.com/2022/05/13/el-salvador-buys-the-dip-again-and-purchases-500-bitcoin-btc-amid-crypto-crash/

https://cointelegraph.com/news/el-salvador-bitcoin-wallet-shows-strong-sign-of-adoption-exec-says

https://research.ark-invest.com/hubfs/1_Download_Files_ARK-Invest/White_Papers/ARK_BigIdeas2022.pdf?hsCtaTracking=217bbc93-a71a-4c2b-9959-0842b6fe301c%7C2653a4d0-af35-42f0-853a-c5f90f002abb

OTHER READS

ECB: The digital economy, privacy, and CBDC: https://www.ecb.europa.eu//pub/pdf/scpwps/ecb.wp2662~fa8429a967.en.pdf

ECB: Central bank digital currency and bank intermediation: https://www.ecb.europa.eu//pub/pdf/scpops/ecb.op293~652cf2b1aa.en.pdf

BLOCKZERO IN THE COMMUNITY

Arun Balu Pazhayannur, Manager at BlockZero, had the opportunity to provide an interview with the Finance Story on his life story and on what BlockZero does.

Overview of Digital Assets

Organized by: CA Finance Story

Audience: Finance and Accountants globally

Duration: 30 min

Key message: BlockZero provides niche digital asset consulting for firms interested in the evolution of their financial infrastructure.

Link: https://www.thefinancestory.com/engineer-turned-chartered-accountant-arun-pazhayannur-joining-crypto-space

WHO ARE WE:

BlockZero is a boutique consulting firm specializing in the evolution of the financial infrastructure through digital assets, digital currency, stablecoins and Central Bank Digital Currency (CBDC).

BlockZero advises global financial institutions, central banks and financial technology companies in the exploration, experimentation, technical implementation and rolling out of digital asset-based infrastructure.